Bank Data Destruction is a regulatory and risk-management requirement, not an operational cleanup task. Banks and financial institutions manage account records, transaction histories, loan files, customer identifiers, and internal financial data that remain sensitive long after systems are retired. When devices leave custody without verified outcomes, the exposure remains with the institution.

Effective handling of end-of-life devices must eliminate that exposure through verification, traceability, and defensible reporting. Financial Institution Data Destruction is executed through controlled processes where proof, not assumption, determines the outcome. If Financial Data Destruction cannot be verified, the device is scrap and the only acceptable result is certified physical destruction.

This standard applies consistently across Laptop Data Destruction, Hard Drive Destruction, and all other data-bearing devices handled within banking environments.

Any outcome outside this framework leaves institutional exposure unresolved.

Data obligations do not end when banking hardware is decommissioned. Bank Data Destruction must withstand regulatory examination, internal audit, and incident review. Lock status, encryption claims, and resale intent do not satisfy examiner expectations. Only verification closes risk.

Failures in Financial Institution Data Destruction expose banks to customer harm, regulatory penalties, and reputational damage. Responsibility does not transfer when devices are handed to third parties.

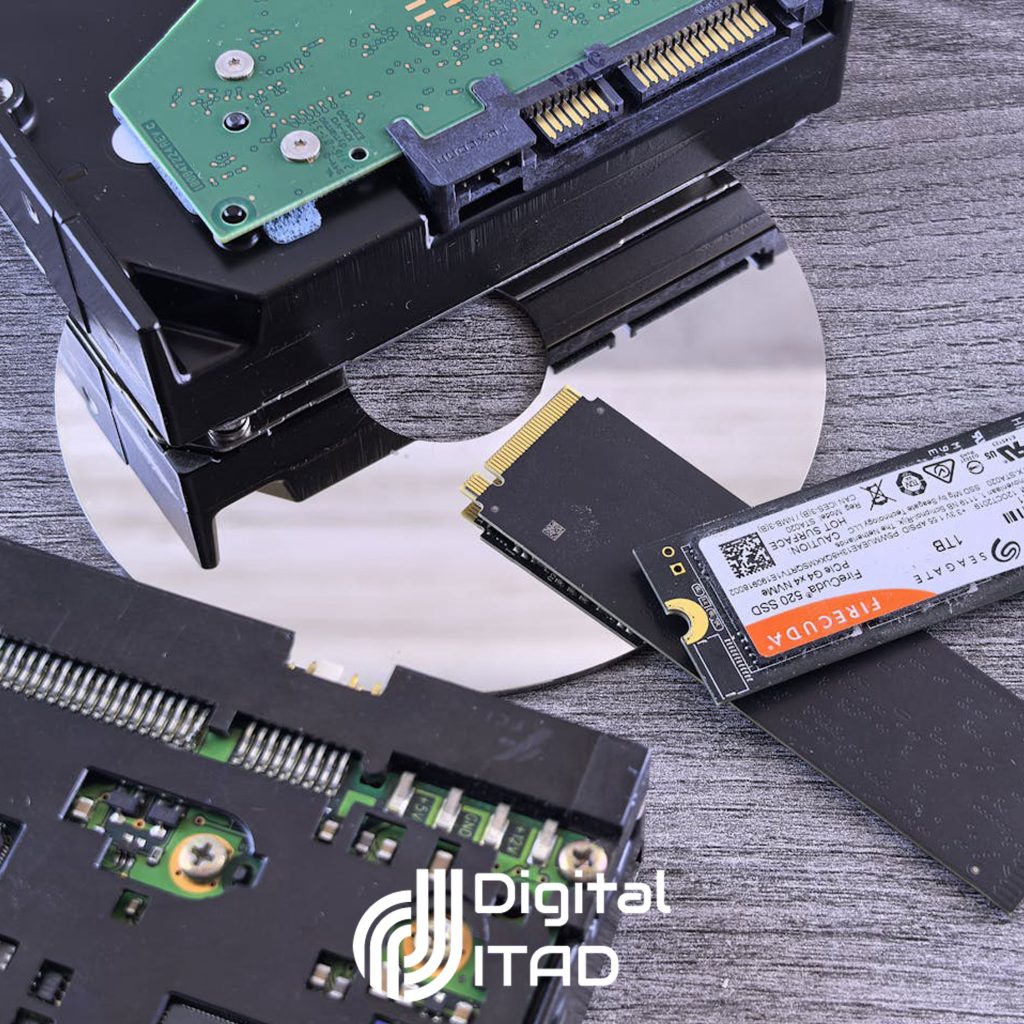

Hard Drive Destruction is often the required outcome for Bank Data Destruction and Financial Data Destruction. Storage media concentrates risk, and wiping cannot always be proven sufficient.

Unit-level tracking and documented proof govern Hard Drive Destruction. Whenever wiping cannot be verified or absolute certainty is required, destruction is mandatory.